Banks are ranked by most recent financial data, revenue, assets, earnings, market value. TD Bank data is from the February to July 2012 period. % change in market value over the last year represents the change in total market value. When USA, NYSE, or ADR is shown it means the stock value was already in USD. Just missed the list: Unicredito Italiano (Unicredit Group), Assicurazioni Generali (Generali Group), Royal Bank of Canada.

A lot has happened since my last report on the banks exactly one year ago. In May 2012 JP Morgan's CEO announced that faulty derivatives trading caused the bank to lose more than $2 billion. The news sent the stock reeling, in after hours trading that day the company lost more than 11% of its market value. The loss is significant because that's about the same amount of market cap that separated it from the other top valued financial institutions.

Canadian banks are aggressively pursuing acquisitions ! Between 2008 and May 2012 Canadian banks spent $37.8 billion on ~100 acquisitions which is impressive considering big banks like Citibank and BNP Paribas were trying hard to sell off assets. To put things into perspective, between 2001 and 2008 Canada's six big banks spent $38.0 billion on acquisitions meaning that today they are spending at roughly twice the rate they used to. One thing to consider though is the fact that a lot of their recent acquisitions bolster their position in Canada rather than overseas; 95% of the purchases they made between 2001 and 2008 were abroad. So far in 2012 some of the biggest Canadian deals were made by TD Canada (acquisition of MBNA Canada) and more recently the Bank of Nova Scotia (August 31, 2012 closes deal with ING Groep for ING Canada, paying only $1.9 billion net in cash for 3% of the Canadian market for retail banking). ING used the money to help pay off a government bailout it received a few years ago. That's pretty much it for ING in Canada, if you remember, back on May 13, 2009 ING sold all of its share in ING Insurance to institutional investors for $2.2 billion. Today, that 70% share is worth about $5.5 billion. Why is ING so eager to get out of Canada ?

In China, payment delays are becoming more problematic especially in the mining sector (debt owed to machinery companies up significantly). That's causing headaches for the big four banks there which have seen their market capitalization drop off quite a bit from last year's highs. More of the loans on their books are becoming risker and investors are taking notice.

Royal Bank of Scotland: I excluded it from my list last year and again this year. This year the bank's problems go beyond just the unending quarterly losses. The company's market value remains pennies on the dollar at just over US$20 billion which is lower than it was at this time last year. The bank remains mired in problems which include conflicts of interest, rigging of inter-bank borrowing, IT malfunctions, problems in Ireland. The bank's market cap has been erratic as of late. It's also 83% owned by the British government.

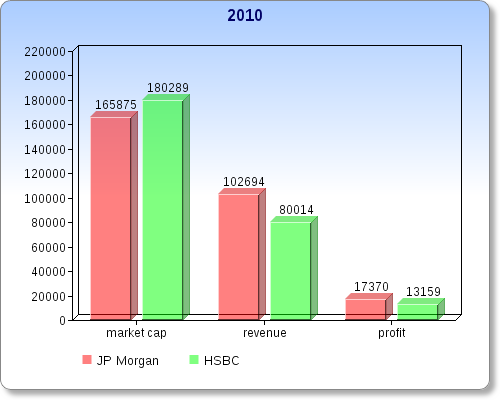

World's 21 leading financial institutions with data from last six months as quoted in company reports (using domestic currency): click on link for company interim 2012 report (in the case of TD Bank it's the 2nd + 3rd qtr ending July 31, 2012)

| Bank | Assets | Revenue | Net Income | ||||||

|---|---|---|---|---|---|---|---|---|---|

| June 2012 | June 2011 | % chg | 1H12 | 1H11 | % chg | 1H12 | 1H11 | % chg | |

| ICBC | 16,431,196 (mar'12) | 14,896,048 | +10.3% | 258,900 | 231,160 | +12.0% | 123,200 | 109,600 | +12.4% |

| HSBC | 2,652,334 | 2,690,987 | -1.4% | 43,672 | 42,311 | +3.2% | 9108 | 9762 | -6.7% |

| ConstrBank | 13,505,745 | 11,754,766 | +14.9% | 227,812 | 197,246 | +15.5% | 106,494 | 92,953 | +14.6% |

| JP Morgan | 2,290,146 | 2,246,764 | +1.9% | 48,232 | 52,000 | -7.2% | 9884 | 10,986 | -10.0% |

| AgriBank | 12,112,888 | 10,725,141 | +12.9% | 210,780 | 184,633 | +14.2% | 80,522 | 66,679 | +20.8% |

| BO China | 12,825,590 | 11,483,498 | +11.7% | 179,665 | 165,974 | +8.2% | 75,002 | 70.234 | +6.8% |

| Citigroup | 1,916,500 | 1,956,600 | -2.0% | 38,048 | 40,348 | -5.7% | 5877 | 6340 | -7.3% |

| BO America | 2,190,868 | 2,338,826 | -6.3% | 44,246 | 40,113 | +10.3% | 3116 | -6777 | up |

| TD Bank | 806,283 | 713,642 | +13.0% | 11,591 | 10,540 | +10.0% | 3396 | 2894 | +17.3% |

| Itau Unibanco | 888,809 | 793,679 | +12.0% | 40,183 | 35,821 | +12.2% | 6729.8 | 7132.5 | -5.6% |

| Santander | 1,292,677 | 1,231,908 | +4.9% | 22,544 | 21,403 | +5.3% | 1704 | 3501 | -51.3% |

| AIG | 555,383 | 610,427 | -9.0% | 35,566 | 34,119 | +4.2% | 5788 | 3554 | +62.9% |

| BNP | 1,970,041 | 1,983,154 | -0.7% | 19,984 | 22,666 | -11.8% | 5082 | 5246 | -3.1% |

| Goldman Sachs | 948,638 | 936,910 | +1.3% | 16,575 | 19,175 | -13.6% | 3071 | 3822 | -19.6% |

| UBS | 1,412,043 | 1,419,162 | -0.5% | 12,934 | 15,515 | -16.6% | 1252 | 2822 | -55.6% |

| Lloyds | 961,371 | 978,951 | -1.8% | 8,965 | 10,868 | -17.5% | -641 | 2278 | up |

| Barclays | 1,631,265 | 1,492,922 | +9.3% | 15,475 | 15,299 | +1.2% | 480 | 1983 | -75.8% |

| Deutsche | 2,241,174 | 2,164,103 | +3.6% | 17,214 | 19,014 | -9.5% | 2063 | 3363 | -38.7% |

| ING Groep | 1,237,248 | 1,240,731 | -0.3% | 7,759 | 7,137 | +8.7% | 1851 | 2888 | -35.9% |

| IntesaSan | 666,417 | 644,673 | +3.2% | 8944 | 8720 | +2.6% | 1274 | 1402 | -9.1% |

| SocGen | 1,246,666 | 1,158,008 | +7.7% | 12,583 | 13,122 | -4.1% | 1405 | 1897 | -25.9% |

Highlights and Some Key Data To Keep In Mind:

Industrial and Commercial Bank of China

Revenue growth outpaced growth in operating expenses (13.7% vs 12.6% for the half) and that pushed the cost to income ratio down to 25.57% which is a first half record low. EPS 0.35 RMB up from 0.31 RMB qoq.

On July 6, 2012 ICBC announced the closing of the acquision of 80% of the Bank of East Asia, a deal that gave it a foodhold in the US market.

By June 30, 2012 ICBC middle east operations already surpassed their 2011 full year earnings.

S&P has a slightly higher rating of the bank vs Moody's (outlook positive vs stable).

June 2012: ICBC is present in 34 countries, overseas asset value at US$ 166.6 billion +33.6% since December 2011.

Banco Santander

Profit from continuing operations was €3472m down only 11.9% from (€3940m). The real profit decline of 51.3% --> €1704m is due to the setting aside of €1,304 million in the 2Q12 in provisions for property (real estate exposure in Spain); That reduced 2Q12 net income from €1,404 million --> €100 million.

American International Group Inc. AIG

Insurance premiums contributed 53.6% of revenue ($19,080m / $35,566m) which is down from 56.8% in 1H2011 ($19,380m / $34,119m)

Deutsche Bank

In euros, assets (+3.56%) and deposits (+0.61%) went up in value but because the euro lost -8.19% of its value relative to the USD when denomited in dollars both experienced a decrease in value.

Societe Generale

Asset value actually went up +7.66% however the euro lost -8.19% of its value relative to the USD and that caused SocGen asset value to fall slightly when denominated in dollars.

Agricultural Bank of China Breakdown of Customer Deposits

June 30, 2012: 53.4% are demand deposits (28.3% individuals / 25.1% corporate), 41.4% time deposits (39.8% individuals / 11.6% corporate), rest are other.

June 30, 2011: 57.4% demand deposits (28.6% individuals / 28.8% corporate), 38.9% time deposits (28.7% individuals / 10.2% corporate), the rest are other.

Revenue is quoted as operating income, customer deposits are referred to as Due to Customers.

China Construction Bank

EPS basic and diluted are the same, 0.43 rmb up from 0.37 rmb

The bank's cost to income ratio down to 32.73 from 36.19 year ending December 31, 2011

Customer deposits breakdown: June 30, 2012: 51.2% are demand deposits (18.3% personal / 32.9% corporate), 48.8% time deposits (27.9% personal / 20.9% corporate), rest are other.

June 30, 2011: 53.5% demand deposits (18.5 personal / 35.0% corporate), 45.2% time deposits (26.7% personal / 18.5% corporate), the rest are other.

Toronto-Dominion Bank

TD's 3Q2012 was one of the best on record; EPS (basic) up to $1.92 from $1.84 in 2Q2012, $1.77 in 3Q2011. Though the company's bottom line was much improved, it didn't result in any dividend hikes (still at 0.72 q2q, but up from 0.66 last year).

For the recent third quarter wealth and insurance net income was +3.15% --> $360 million (21.1% of total group profit).

In just the last 3 months TD's total assets are up +4.28% !

Revenue grew +1.6% between April 2012 (2q) and July 2012 (3q) compared to 5.2% between April 2011, July 2011.

Only 16% of its wealth and insurance net income comes from its ~ 30% stake in TD Ameritrade.

In 2012 TD acquired MBNA Canada.

About the table at the top of the article, currencies used*Average fx rate calculated myself using data at x-rates.com and google finance exchange.

Exchange rates used to convert to USD for the 6-month period (used for customer deposits, revenue, net income/profit)

Chinese RMB 1hfy12 0.158243255555, 1hfy11 0.1529334634 up 3.47%.

Euro 1hfy12 1.29745937777, 1hfy11 1.403703906 down 7.57%.

Swiss Franc 1hfy12 1.07705781666, 1hfy11 1.10659625 down 2.67%

Brazilian Real 1hfy12 1.86424560555, 1h11 1.6312765625 down 14.28%.

British Pound 1hfy12 1.57693847777, 1hfy11 1.61702795275 down 2.48%.

Canadian Dollar 1hfy12 1.00605145856, 1hfy11 0.9704058232 down 3.67%

Currencies used for assets last day of most recent reporting period

Chinese RMB June 30: 2012 6.3550, 2011 6.46350

March 31, 2012 6.29700 (ICBC)

Euro June 30: 2012 1.266350, 2011 1.451931

Swiss Franc June 30: 2012 0.947650, 2011 0.84160

Brazilian Real June 30: 2012 2.00950, 2011 1.560491

British Pound June 30; 2012 0.636679, 2011 0.62250

Canadian Dollar July 31: 2012 0.955100, 2011 0.955100