Even with a collapse in oil prices Canadian oil production - driven by activity in the oilsands, is expected to increase by 150,000 bpd this year and by that same amount again next year. Canadian Association of Petroleum Producers

According to ARC Financial, the number of wells drilled in Western Canada will be down 50% this year as compared to last (5,300 vs 11,222). Though production keeps rising, companies remain burdened with higher than acceptable costs.

- estimates suggest as many as 30,000 workers have lost jobs in Canada’s oil and gas industry since the downturn began last fall.

- low-cost oil reserves in Saudi Arabia vs high cost reserves in Alberta (Alberta oil) and us shale (North Dakota shale)

- Canada’s reserves may be as massive but they are much more expensive to extract from

- This appears to have had more of an effect on producers south of the border (where shale exploration has officially stalled) than in Canada .. Canadian companies have huge cash reserves which they are they able to dip into when prices get too low .. and so they are able to fund core projects until new cost cutting measures take effect.

According to the latest quarters as of May 2015 company earnings are way down - earnings losses mount in Canada

Suncor Energy Inc (SU) - 1Q15 $(341) million loss or 24 cents per share vs $1.485 billion or 101 per share in the previous year.

Oil Sands operations production was 440,400 bbls/d in the first quarter of 2015, compared to 389,300 bbls/d in the prior year quarter, primarily due to minimal maintenance activities in the first quarter of 2015. Production highlights included 346,500 bbls/d of SCO due to strong upgrader reliability, and record production of 188,700 bbls/d at Firebag. Cash operating costs per barrel for Oil Sands operations decreased in the first quarter of 2015 to an average of $28.40 per barrel (bbl), compared to $35.60/bbl in the prior year quarter, due to increased production and lower costs as a result of lower natural gas prices,Suncor's share of Syncrude production of 35,200 bbls/d in the first quarter of 2015 remained comparable to the prior year quarter production of 35,100 bbls/d.

UK has lowered its tax rate on oil profits made in the North Sea ! At suncor this saved the company $406 million (62-> 50%).

Cenovus Energy Inc (CVE) - Oil Sands production is up 20% (to 144,000 bpd) but the company endured a massive $668 million quarterly loss recently attributable to the decline in the realized price of oil and natural gas (-47% -> $37.66; -25%-> $4.47). In the quarter just prior to this one the loss was $472 million.

Top Producers of Shale in North Dakota (Bakken)

- Whiting Petroleum Co. (NYSE: WLL) - quarterly production 1.6 million barrels (19% of company production)

- Continental Resources Inc. (NYSE: CLR) - 127,788 bpd

- Hess Corp. (NYSE: HES) - 63,000 bpd (85% of company production)

- Statoil ASA (NYSE: STO) - 50,000 bpd (9% of company production)

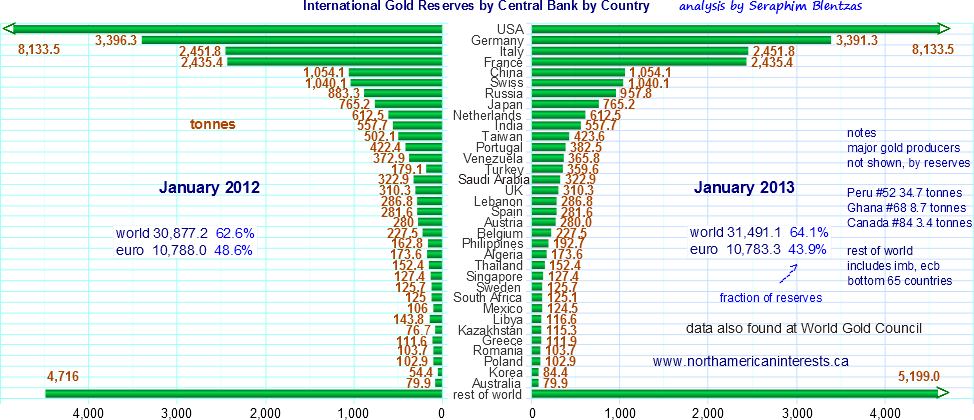

China Revises Gold Reserves (October 2015: China reserves)

- First time in four years China says anything about its reserves

- According to Wood Mackenzie China has 30,000 tonnes of gold, more than any other country.

Since the middle of the last decade China has been leading all countries in terms of gold output - very little of that actually leaves the country.. add to that the fact that China imports another 1000 tonnes of the yellow metal through various ports (HK being the largest) and you can start to see the potential it has to accumulate massive reserves.

- Gold withdrawals from the Shanghai Gold Exchange hit a record high of 620 tonnes in the first three months of 2015.

- Private consumption in China is probably not that high meaning at least a portion of that is going to China's central bank. Current estimates put China's reserves at just over 1000 tonnes, far behind the top four countries which have a combined 16,500 tonnes.

- According to various sources out of China, the upcoming report will act to bolster China's currency - This gives foreign currency traders (and governments) more confidence in the yuan-renminbi as an alternative to the US dollar.

- China and Brazil have already signed a $30 billion currency swap agreement.

{kind=link}

{kind=link}