If the first two months are any indication, 2012 will be a very busy year for investors. Just when you think you're ahead of the game some external, unaccounted-for factor changes everything. It can be reassuring though, knowing that everyone has to adjust their portfolios accordingly. Take for example the airline industry;

Over the last month (Feb - Mar) the price of WTI oil shot up 11% from just under $99/bbl to $109/bbl. Consequently, brent crude hit a 43-month high of $128.40/bbl on March 1, 2012. How did that affect airline stocks? They were BATTERED more than the fish at Red Lobster! Over the last month United Continental Holdings Inc (nyse:UAL) was -16%, Delta Air Lines (DAL) -14%, Lufthansa (DLAKY) -7%, negatives across the board all because of the price of oil. What's more, oil could soar even higher if Iran chooses to close the Strait of Hormuz because the Strait is used to transport 7% of the world's oil; Closure of the Strait of Hormuz is entirely possible now given that Europe has implemented an embargo on Iranian oil (supplied 4% of Europe's demand last year) and that it's already dealing with the toughest sanctions the West can impose on it (Iran is now demanding payment for its oil

in gold). sidenote: India is one of a few countries that still imports oil from Iran.

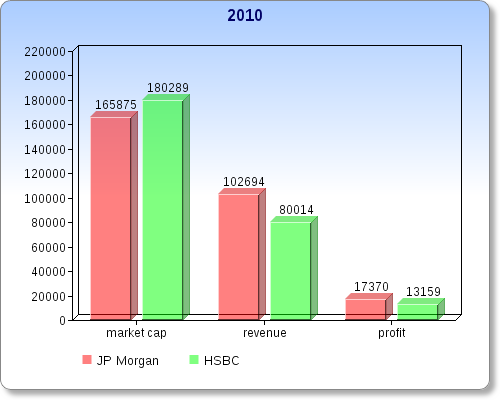

Canadian bank stocks proving their value once again ! The two largest by size, Royal Bank of Canada (RBC) and Toronto-Dominion Bank (TD) raised dividends despite profits being lower. At RBC the dividend increase was 5.6% bringing it up to 0.57/share in the latest quarter (eps was down 4.7% to $1.21/share). At TD, the 1Q2012 showed mixed results. Though TD earnings dropped marginally (-0.01/share to $1.55) revenue grew 3.3% to $5.64B. Though profits did not grow the bank continued to hand out larger dividends (+4c quarterly to 0.72).

Also making news is SNC-Lavalin. Partnered with Aecon, SNC won a $600M contract to refurbish Ontario, Canada's Darlington nuclear station. That pushed the stock up 2.2% in just the last day helping it to climb over the $6B level of capitalization. Prior to the news, the stock was reeling (lost $1.6B about 1/5th of its market cap in just the last couple days) because of reports of undocumented payments unrelated to company projects eroding away at 2011 profits.

The World is Producing More Gold but also Consuming More (led by China, Germany and Thailand)

In 2011, 11 of the world's 14 leading gold producing regions raised their output according to the US Geological Survey's

2012 Mineral Commodity Summaries, which isn't surprising considering the

28% jump in gold price (and cash costs, accordingly). On the year, world primary production was up 5.5% to 2700 tons (86.4M ounces). The world's 14 major producers accounted for 76.7% of output down from 78.2% in 2010. Although production in China was higher, the growth was not as great as it had been over the last couple years (+2.9% compared to +22.0% for #8 Ghana, +20.9% for #7 Canada and +16.4% for #11 Mexico). South Africa is home to 11.8% of the world's gold reserves (2nd overall behind Australia) but was the source of only 7% of production in 2011 bringing its overall rank down to 5 from 1 in 2007. Why the drop for South Africa? Because of ridiculously high production costs; South Africa has the unfavorable

distinction of being the most expensive country to produce in (among major producing regions).

When investing in gold mining companies be sure to have companies with projects in Australia high on you list (ie BHP Billiton - Olympic Dam). Australia was the source of only 10% of global production last year but is home to 15% of reserves meaning growth will happen. Production costs (South Africa) and barriers to entry (China) are also not as problematic in Australia. In late 2011 China began drafting new standards for the gold industry which could have a significant effect on both investment and production in the country.

Most of China's gold output comes from small companies but the

new standards will eliminate some of them while at the same time, making it more difficult for new companies to enter the industry.

With regards to the

United States, the gold supply and demand situation there is not as dire as one would expect. In 2011 GOLD CONSUMPTION ACTUALLY FELL -17% to 194.9 tonnes (2nd consecutive year that US gold demand dropped). That's in stark contrast to China (+22% to 811.2 tonnes) and

Germany (+26% to 159.3 tonnes). Global consumption of gold in 2011 was 4067.1 tonnes, highest since 1997. Interestingly in Thailand (#7 consumer) where total consumption grew +57% to 108.9 tonnes, jewelry only accounted for 3.8% of the total (fell 34% on the year) but bar and coin demand +66% to 104.8 tonnes. The top six consumers remained the same,

Investing in gold: Mining Companies

Did you know? Mining companies are actually LOSING CAPITAL TO ETF'S ! According to Bank of Montreal analyst Peter Miller ETF's are a "hoover of capital and competition for the gold companies". To regain investor confidence (and capital) many producers are hiking up dividends. I think that mining stocks present a unique opportunity for investors at the moment. Yamana is raising quarterly dividends by 10%.

With regards to gold producers, 2011 wasn't as profitable as one would expect. At Newmont Mining and Goldcorp, 2 of the 4 largest by market cap, net earnings were lower despite record breaking revenue. Part of the reason has to do with rising cash costs; +12.5% to $460 at Barrick Gold, +20.5% to $591/oz at Goldcorp (though lower from $270 to $223 when by products are taken into account), +40% at Australia's Newcrest, since 2009 +29.7% at Yamana Gold. Higher mining costs are atributable to increasing equipment, labor and raw material costs. Higher gold and silver prices buffered the effects of higher costs however companies need to do more to translate sales growth into earnings growth. The higher gold price allowed even AngloGold Ashanti to add to reserves; Anglogold's reserves went up 4.4M ounces bringing the total to 75.6M ounces; 3.7M of the 4.4M oz added came due to higher prices making extraction from ore at Vaal River economically viable (3.2M oz) and 0.5M oz attributable to improved ore reserve price at Geita.

South America increasingly important to major gold miners - Gold Fields will get 20% of its 2015 gold production from that region, up from 10% in 2011, 2% in 2008. In 2011 Gold Fields produced 3.697m ounces of gold which is 4.0% less than in 2010 (3.851m ounces) but it did receive 28.6% more for each ounce of gold ($1569 vs $1220). Barrick Gold's huge project Pascua Lama is in Argentina. Goldcorp's largest venture is the Penasquito mine in Mexico.

Undervalued Mining Companies

Seabridge Gold (tsx: SEA) - In February released its 2012 Operations Overview and the new data is impressive to say the least (maybe that's why the stock is UP +8% since February 13, still down though over 20% last 6 months because of increased volatility in metal prices (even Barrick Gold is down 10% over six months). Its flagship project, KSM has 2P reserves of 38.5M ounces for gold, 9.985B pounds for copper, 214M ounces of silver and 257M pounds of molybdenum; That means it has more gold than world renown projects Pueblo Viego, Penasquito and possibly even Ivanhoe Mine's mega project Oyu Tolgoi (46.4M ounces of gold) if KSM reserves are increased in April which is likely given the successful M&I drilling results reported by the company on February 8, 2012. Reserves in situ value is about 15% greater than Goldcorp's Penasquito and Seabridge's enterprise value per ounce of reserves is only $21 ! which is ridiculously low considering it's $1200 at Canada's other major gold junior-mid cap company AuRico. At Detour Gold and Osisko Mining enterprise value/oz is around $400. Don't forget that KSM isn't the only major Seabridge project, there's also Courageous Lake (8M oz M&I 16 year mine life). Because reserve grade is relatively low the company will benefit from rising metal prices moreso than say Yamana Gold.

The same month, on February 8, 2012 measured and indicated resources at KSM improved by 3.7 million ounces for gold (to 49.0 million ounces) meaning that drill results continue to be successful. What it also means is that the company's next report on proven and probable reserves (April 2012) will likely indicate further increases in 2P reserves, past the current estimate. In the February report, Seabridge Gold estimates annual production at KSM will be 854,000 ounces (gold), 166 million pounds (copper), 2.9 million ounces (silver), 1.1 million pounds (molybdenum) for the first seven years (the mine has a 52 year mine life, molybdenum production will actually grow after the first seven years). Base cash cost will be $231/oz which is even lower than Goldcorp ($300).

This company screams undervalued.

How does a company with 40M ounces of 2P gold reserves (more than Yamana Gold, Agnico-Eagle Mines) at just one of its projects have a market cap under $1 billion ? Royal Gold has shown confidence in the company's numbers (invested $100m in Seabridge last year). The construction costs remain quite high but I think that $2000 gold (when it happens) will open up more financing options (like Eldorado Gold recently got from Qatar Holdings). Consider this: 2 years ago when gold prices were a lot lower, Barrick Gold paid Kinross Gold $475m ($455m cash) for 25% interest in the Cerro Casale gold copper project which has only 60% as much gold as KSM. That would value KSM at over 3X Seabridge Gold's market cap at present.

Hecla Mining Company (nyse: HL) - On January 11, 2012 Hecla announced that the Lucky Friday Mine in Idaho which produced 31.5% of the company's 9,498,337 ounces of silver in 2011, will be shut down for the entire 2012 year. The day of the announcement the stock fell 18.7% from $5.67 --> $4.61. All this because of a December 2011 accident at Lucky Friday in which a number of employees were injured when the mine collapsed (including a couple fatalities). You can be sure that whatever structural problems caused the collapse will be dealt with quickly (only two months was needed to fix the problem, the 12 month closure is due to new inspections and safety procedures required by federal regulators; A group of shareholders even tried to sue the government over the closure). Hecla wasn't the only miner that suffered fatalaties last quarter, 6 people died in accidents at three AngloGold Ashanti mines.

Though Lucky Friday is the source of only 31% of silver output (0% for gold) and 30% of 2P silver reserves, it's Hecla's only source of proven silver reserves (~21 million ounces); In 2011 it was the source of all of Hecla's total increase in 2P silver reserves (+7 million ounces), so it remains a significant growth project for the company. Lucky Friday also makes the company more diversified, being home to three-quarters of its 1.5 million ton lead resource. The other operating mine, Green's Creek was purchased from Rio Tinto in 2008.

There are many reasons to like Hecla Mining

* The price of silver jumped 74.2% in 2011, single handedly causing Helca's profit to grow 286% to $150.6M. Revenue reached a record high of $477M even though it sold 13.3% less silver; in fact sales of all four metal types were down (-17.5% for gold, -16.6% for lead, -12.4% for zinc). The company's stock value is down -50% from a year ago even though revenue and profit is up significantly; Even considering the 30% drop in silver production, next year company profits probably won't be less than they were in 2010 with high commodity prices a mainstay.

* The company has no debt and nearly $290M in cash and cash equivalents.

* Lucky Friday structural damage only needs two months to fix.

* Hecla Mining has three other significant projects at San Sebastien, San Juan and Noonday. Company's valuation at present definitely isn't giving any of those projects respect.

Thompson Creek Metals (tsx: TCM) - The stock has been in selloff mode for the better part of a week after the company reported that the Mt. Milligan project will cost more than previously thought. That prompted TD Bank to downgrade it.

Barrick Gold - Pueblo Viejo (60%) and Pascua Lama mines will begin producing in 2012/2013. When fully operational (2016) the mines will

add 1.5 million ounces of annual output to Barrick Gold's current production of 7.68 million ounces. Pueblo Viejo is 90% complete. Barrick profited 25% more in 2011 than it did last year ($4.48 billion, $$4.67 billion adjusted). In February Barrick exited Russia when it sold off its last remaining asset there (25% interest in Highland Gold).

Goldcorp - 2011 production was 2.5147 million ounces. By 2016 production will rise to 4.2 million ounces. Revenue grew by 43% in 2011 more than any other top 10 gold miner. El Morro in Chile ($3.9b project) is one of the reasons for the higher output projection.

Newcrest Mining - 515,000 oz of gold in 2011 came from the Telfer mine representing about 20% of company total (Telfer is home to 14.9% of its 79.1M oz of reserves, 7.7% of the 8.36M tonnes of copper reserves). Total company production in the 2Q2012 FY (ending December 2011) was 579,023 oz down 19.9% qoq, the quarter before that 1Q2012 output was down 16% to

587,296 oz. Over the last two quarters production from Telfer was down 50,000 oz. 2011 calendar year production increase comes entirely from the Lihir Gold acquisition.

Kinross Gold - Yes it was hit with a $2.94 billion impairment charge stemming from an unexpected writedown on its Tasiast mine in Mauritania absorbed during the fourth quarter of 2011. That effectively more than wiped out any profit the company was on track to make in 2011 (ended up losing just over $2B on the year). But keep in mind the company's revenue (+31%), gold production (+13.0% to 2.6M oz), and cost of sales (+28% even though production up more than 30%, production cost of sales up 17.7% to $596/oz which is comparable to its peers in the industry). Another telling statistic: cash margins up 32% to $906/oz ($965 in 4Q +23%), margins were also up 32% at America's largest gold miner Newmont Mining (Newmont's stock is up 16% last 12 months, Kinross is down -32% even though Newmont also suffered from a bad fourth quarter; -$1B losses at Newmont in 4Q2011 brining total profit for the year down to $366m). Also to consider; Agnico-Eagle Mines took on a $644.9m writedown on its Meadowbank mine in the 4Q giving the company a net loss of $601.4m in the 4Q. The mine plan had to be changed because of its 'high cost nature'.

Also, annual dividend was up 10% to record high 11 cents a share (though none was paid in the problematic 4th quarter). The company was valued at $19B as recently as May 2011 which is almost 60% more than it is today. That brings its market value per ounce of reserve to a near industry low $130/oz (compare that to Goldcorp's $618/oz at, $708/oz at Yamana Gold). Cash flow from operating activities +40.3% to $1.8093b on the year, convinced yet? Then consider the possible takeover offers. European Goldfields which isn't even producing yet and has only a fraction as much gold as Kinross, recently got $2.5B from Eldorado Gold. Kinross has low cash costs, lucrative projects (Cerro Casale) and a growing revenue stream and that makes it a lot more valuable in a M&A scenario. CAPEX was +163% to $1.6515.

Don't forget that Kinross's current market cap of about $12B is about the

same as it was before it acquired $7B Red Back Mining.

Eldorado Gold (nyse: EGO) - Coming off a record year for gold production (+4% to 658,652 oz), revenue (+33% to $1.042b) and even profit (eps +41.5% to 58c) while dividends more than doubled from 5c a share to 11c. Operating cash flow was also strong, up 40%. AND unlike the other major gold producers total cash costs only went up marginally ($382 --> $405). The European Goldfields acquisition will make it the biggest gold producer in Europe by 2015 (1.5m ounces a year) which couldn't come at a better time; European demand for gold is stronger than ever as is the price of gold.

New Gold (tsx: NGD) - In June 2012 its fourth operating mine will open. That will push company production over 400,000 ounces for the first time. Goldcorp's El Morrow (New Gold's interest is 30%) will reach full production in 2018 which should give the company an additional 150,000 ounces annually.

Newmont Mining - Gold reserves grew 9% in 2011 to 99M ounces a third of which is in Nevada, 17% in Africa. Reserves were 93.5M one year earlier and 91.8M oz December 2009.

Biggest source of attraction at Newmont right now are the dividends, 4Q2011 quarterly dividend up 133% to 0.35 a share.

Also of interest:

-

On March 1, 2012 Newcrest Mining, Australia's largest pureplay gold company began trading on the Toronto Stock Exchange. It will be the 4th largest mining company with a listing in Toronto.

-USA has 3rd highest corporate tax rate in the world.