- The China-Brazil trade corridoor had a compound annual growth rate of 30% during the last decade.

- China accounts for 18% of Brazil's total trade, up from 4% in 2000.

- HSBC has only been in Brazil since 1997 but it is already a significant contributor to the country's economy. HSBC now finances 6% of the Latin American country's foreign trade.

- Using current dollars, median household income in British Columbia, Canada is $68,000 today, down from $72,000 in 1971. (source: CBC) What's alarming about that is the fact that the average home price was only $272,000 which is a lot lower than today's $806,000.

- On November 29, 2011 JP Morgan sold 198.143 million shares of HSBC Holdings stock (1.11% interest in the company) for HK$58.83 a share. That reduced JP Morgan's interest in HSBC to 6.35% down from 7.46%

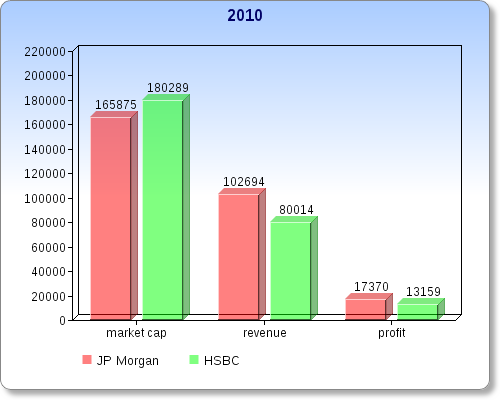

JP Morgan

JP Morgan In 2011, the bank ranked first in terms of global investment banking fees. Though profit was down -22.9% over the last quarter of 2011, total annual profit for the year reached a record high of $19 billion +9.2% vs 2010; Net income per share improved even more, +13.1% to $4.48. During the fourth quarter, non-performing assets fell -33%. Also in the fourth, the bank repurchased $950 million worth of common stock, bringing the total repurchased on the year to $2.9 billion. It's important to remember that, even though JP Morgan has the highest market cap among the top banks (outside China) it remains smaller than Bank of America in terms of employees (260,000 vs 300,000) and revenue ($97.234b vs $115.0b).

What tells me the bank's business is a lot healthier today than last year is the charge-off's vs credit loans; Credit sales volume +10% on the year while consequently net-charge off's happened at the lower rate of 3.93% (down from 4.34%). Deposits are now at $1.1 trillion, +21%. JPMorgan's Investment Bank's provision for credit card losses was up to $272 million at the end of last quarter which compares nicely to the loss of $271 million last year and +54 million in the previous quarter (3Q2011). However it must be noted that, the increased provisions for credit card losses on the year caused net income for the investment bank division to fall by 52% to $726 million.

The commercial banking unit experienced a 21% increase in profit (to $643 million) on record net revenue. Net charge offs down from $286 million to $99 million.

HSBC

Market capitalization down significantly to $136 billion from $180 billion (end 2010) and $199 billion (end 2009). In fact, by the end of the the 2011 calendar year, Wells Fargo pulled ahead of HSBC in terms of market cap (Wells Fargo finished 26 overall, in front of HSBC at 28). Since the financial crisis of 2006-2007, over the last four years HSBC paid out more dividends than any other FTSE100 listed bank except one (US$27.2 billion/ $7.3b in 2011 alone). Dividends were up +14% in 2011. HSBC's costs +10% in 2011 due to, among other things, wage inflation (a new bank fee charged to it by the UK government in the amount of $570m. Underlying costs now account for 61% of revenue up from 55% in 2010). North American operations accounted for only 0.5% ($100m) of HSBC's profit before tax (compared to 2.4% = $454m in 2010).

North American business has become a bit more risky as it now accounts for 22.8% of the company's risk-weighted assets ($337.3m, up from $330.7m in 2010) even though the region represents only 19.7% of total assets ($504m out of $2555.6m). Many of the bank's key financial metrics were up on the year, however there were a couple that weren't; Down were: Underlying profit before taxation: -6% to $17.696 billion, total loans and advancements -2% to $940 million. Good decreases: Ratio of loan impairment chargest to total operating income down to 13.8% from 16.9% in 2010 and 31.7% in 2009.

No comments:

Post a Comment