Gold and Silver Market Ripe For Rapid Growth

Though stateside gold prices may appear docile, from a foreigner's perspective precious metal prices are already too high because in much of the rest of the world the key precious metals have become a lot more expensive to purchase thanks to currency wars : the mighty US dollar.Seventy-five percent of silver production (mine production) happens at gold mines - this means that, when gold production slows down (companies shuttering mines which started happening in the middle of last year) silver output declines. This keeps the gold silver ratio intact despite the delinking of the two metals at London's commodities bourse.

The core price is set by comex, the commodities exchange in NYC and thus is traded in USD.

The fact that the price of both pcm's has barely increased over the past six months in my opinion makes both ripe for the picking !

Elsewhere the strong US dollar is making gold increasingly harder to afford, but that's inflation spurred by changes in local currency rates; though quantitative easing and changes in interest rates are wreaking havoc on other currencies, the USD already has that factored into its value.. with The Fed at its side nothing aside from a shaking of the Fed's basic policy of money creation can shake its value... or of course a tiring by currency traders of the endless excuses for more QE.

In my opinion however, gold should've gained much more than nothing in US dollar terms. Demand is still rising especially among those seeking a tangible hedge against inflation, as well as by those transferring money out of equities in response to growing global economic uncertainty, a shrinking middle class.

The Gold Supply Problem

As of 2014 there is an estimated 24 billion ounces of silver existing in the form of jewelry. Total historic production of silver is about 52 billion ounces, eighty percent of that mined since the dawn of the twentieth century. However, much of the 52b oz will never be available to the bullion market due to its historical value (in the form of religious items, museum pieces, non-scrap jewelry).

India Imports Record Amount Of Gold From Switzerland

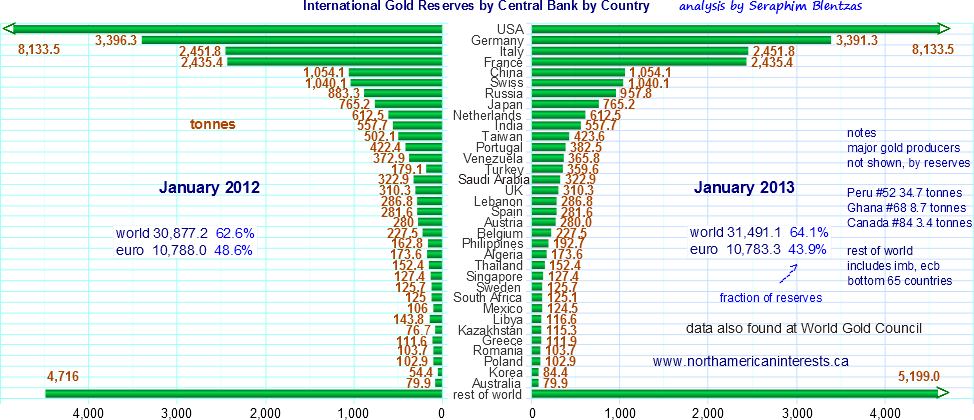

According to data from November 2014 Indian imports of gold from Switzerland totaled CHF2.9 billion up a whopping 600% versus the previous year; it's not just that month either, in October it was up 280%; January through November gold imports amounted to 457 kilos.Russia Continues To Add To Gold Reserves

Russia purchased 20.73 tonnes of bullion in December - note also that in December gold prices were up for the first time in five months (+1%). Makes Russian reserves fifth largest at 1210 tonnes.

Also notable - Ukraine held onto its reserves after selling 16 of 40 tonnes in Oct/Nov.

Then there's the other central banks who cumulatively only became net buyers of gold since 2010 after 20 years of being net sellers.

Russia is key here - July through September 2014 it accounted for 59% of the 92.8t of net gold purchases by central banks. Gold comprises just under 11% of Russian reserves up from 8% in 2013. Those purchases allowed it to leapfrog China (1150 vs 1054).

Gold imports from HK by China were down last year but it was still the second highest on record at 813 tonnes. Demand for gold should continue to increase into February as a result of Chinese new year festivities.

Don't Bet Against The Canadian Dollar !

I don't consider the current CDN/USD fxrate to be sustainable - Beginning in 2016 oil prices are forecast to go up possibly by as much as 50% ($45->$65 per barrel). Also note that Canada's federal government is starting to run a balanced budget while the USA has a severe, structural deficit which ultimately will lead the United States into a situation where it will be forced to run up high payments to foreign bondholders further weakening its long term outlook.Don't Let Yesterday's Gold Selloff Turn You Off

- gold responds positively to durable goods numbers- most global currencies are either under pressure (canada, australia, euro) or being deflated (asia) - this strengthens the US dollar in the near term but makes it increasingly vulnerable over the long term

- when the dollar shows any sign of weakness expect a big jump in precious metal prices

- Greek debt bailout 80 out of 240 billion is owed to Germany - If Greece doesn't pay up Germany will undoubtedly rethink its financial obligations to the Eurozone and that weakens Europe, its central bank and its structure.

{kind=link}